There have been significant changes in consumer dynamics in light of Covid-19 with 2020 turning out to be a year nobody could have predicted. We are all aware of the impact Covid-19 has had on our day-to-day lives, with everything from panic buying in the supermarkets and working from home to high unemployment and school closures.

All of this has led many people to re-evaluate their needs and priorities, for both themselves and their families, especially with the added financial pressure of a recession. What we eat and where we shop has seen a dramatic shift over the course of the year.

Meat purchase habits during 2020

The economic ripple effect of Covid-19 led consumers to re-evaluate their buying behaviours – with price, value for money and buying local becoming more of a priority during lockdown. This led to wider reputational issues such as health, animal welfare and the environment easing off, as factors which consumers had greater control over rose to the surface. However, these concerns are reemerging and it is critical that the meat industry take steps to bolster the reputation of red meat.

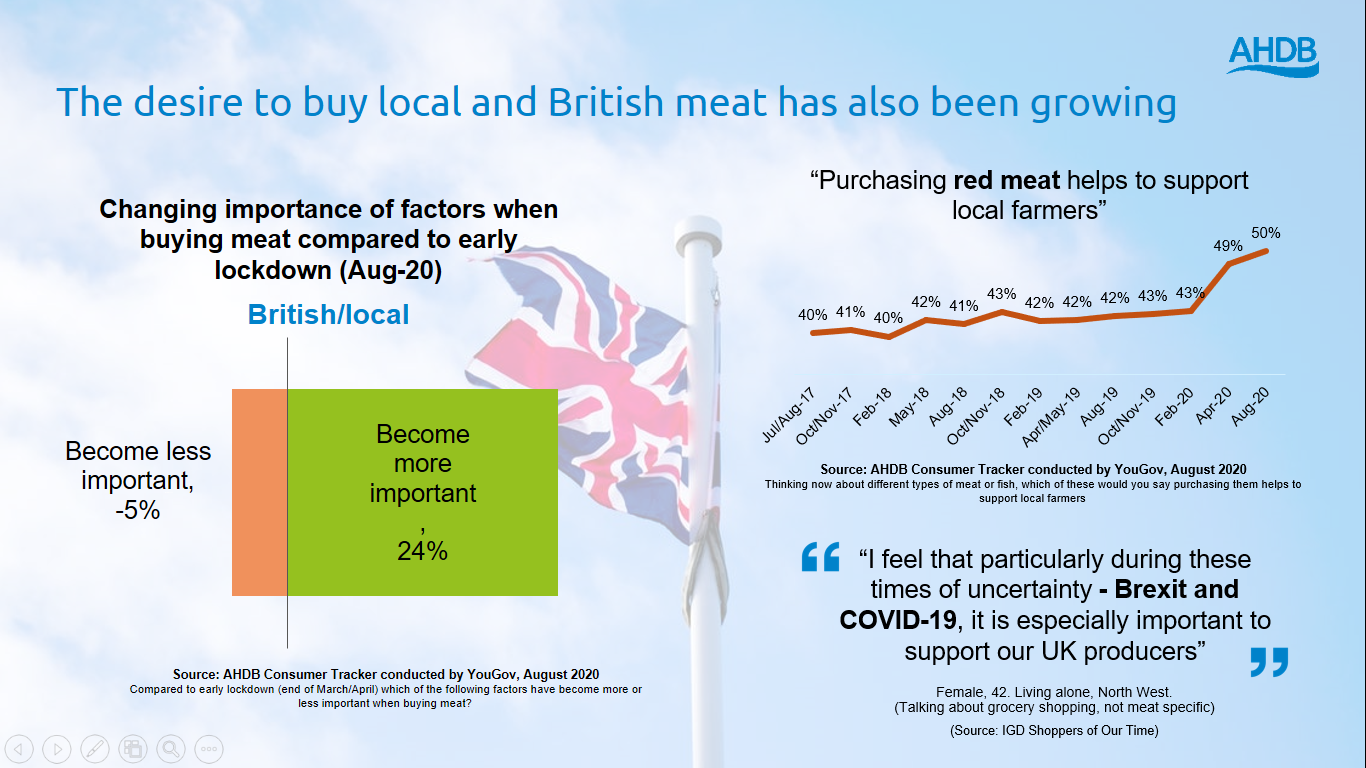

Evidence from AHDB’s consumer tracker research showed that with the pandemic dominating the news, negative media around red meat fell – with fewer people reducing their average consumption of red meat. The desire to buy local and British meat grew during 2020.

But it’s important to remember that simply labelling products as British is not enough to convince shoppers.

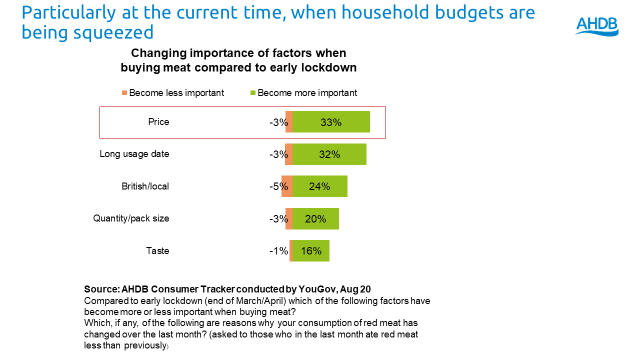

Communicating to consumers on the benefits of local is vital, in particular the quality and trusted messaging that comes from buying British. During the second half of 2020 evidence from AHDB/YouGov Consumer tracker signalled that 33% stated price had become more important to them. This sensitivity to price is likely to be critical to consumers, particularly at the current time, when household budgets are being squeezed.

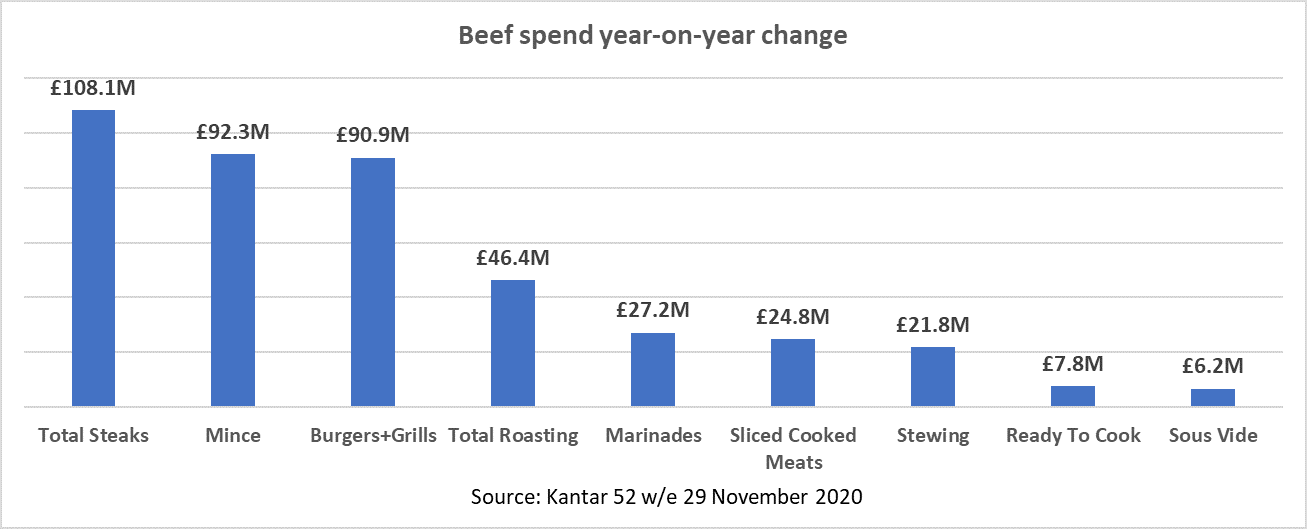

For Beef the largest actual growth in retail spend was around steaks, burgers and mince. These cuts proved popular during a large part of 2020 due to the closure of food-service, resulting in a significant rise in meals cooked in the home.

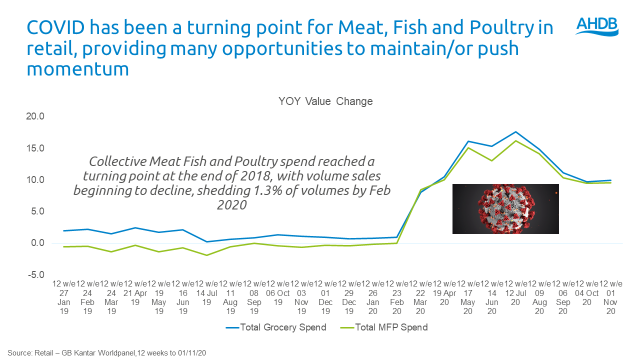

Overall red meat spend across retail outlets increased 12% in the 52 weeks to 29th November (Source Kantar Worldpanel). However, butchers outperformed traditional retail outlets with growth of 22.6% compared to the previous year. While that growth is positive for local butchers, it’s vital they communicate quality and don’t assume shoppers will stay, as the longer-term trend pre Covid was a channel in decline.

Meat and Health

Covid-19 created a health paradox, with many people anxious about the pandemic and its impact on their health, but also feeling a desire to comfort eat. While healthy eating means different things to different people, the top health priority for most consumers was eating more fruit and vegetables.

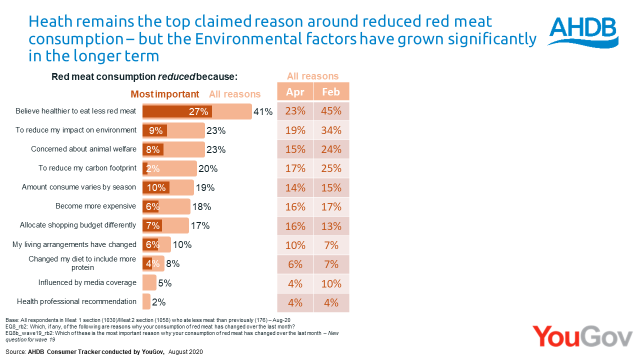

Health remained the main reason stated behind those who claimed to be reducing their meat consumption, with evidence from AHDB/YouGov Consumer Tracker showing this as a critical topic for consumers. While ‘health’ dipped in intensity as a claimed reason for reduction during April 2020 (23%) it did bounce firmly back in August (41%).

During significant periods of 2020, there were signs that consumers were thinking more about comfort than health and choosing traditional meals that they associate with good, hearty dinners for the whole family. In the longer term with the government’s new obesity strategy being proposed, some red meat products such as back bacon and 20 per cent beef mince, could be impacted, both in retail and out of home.

This all highlights the importance of communicating the nutritional benefits of red meat to ensure the sector remains in a strong position now health concerns are starting to reemerge.

Consumers and the Environment

On balance, most consumers believe farmers care about the planet with 64 per cent in agreement (AHDB/Blue Marble Trust Research 2020). And with more people buying local this year, farmers and independent retailers have a great opportunity to capitalise on shoppers’ approval ratings.

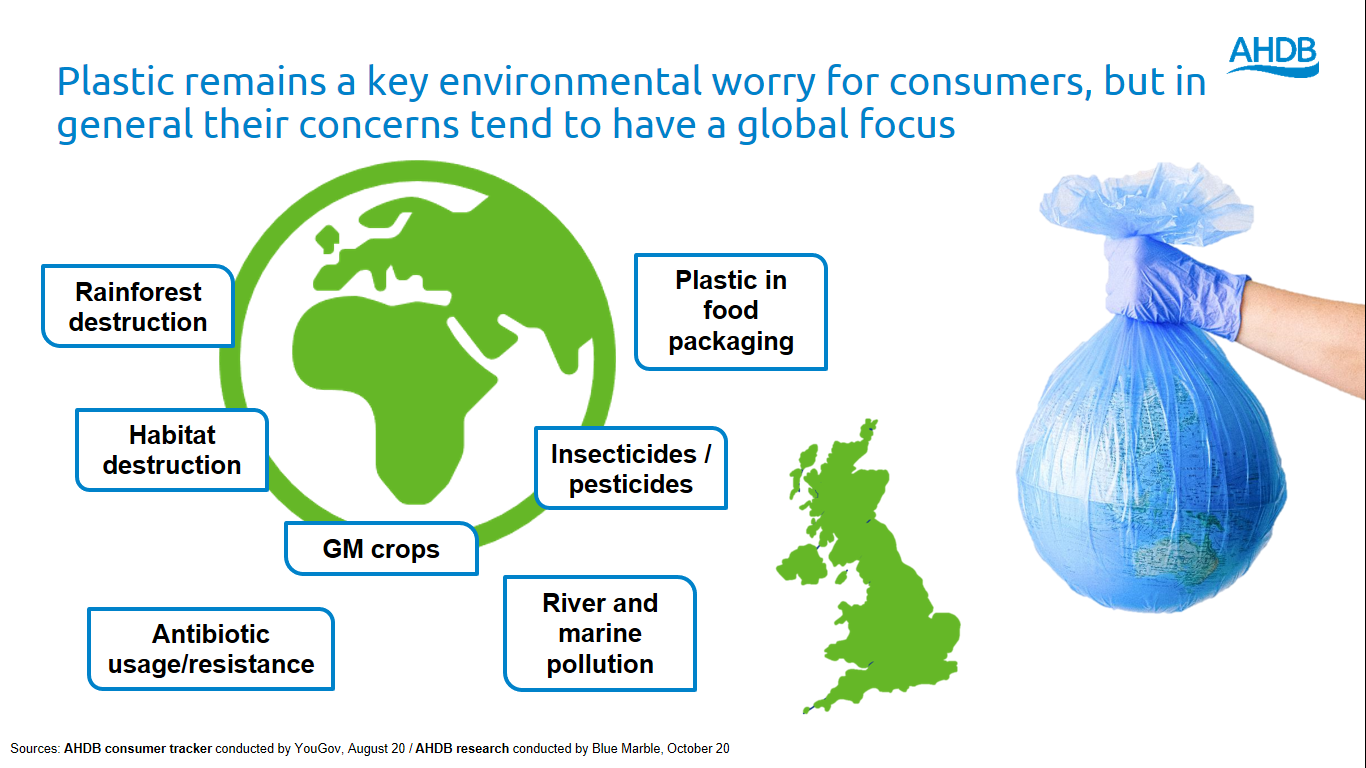

When it comes to what people can do themselves, issues such as food waste and plastics are top concerns. There are lots of different exposure points for consumers on environmental messaging, with many consumers finding it confusing in regards to what is global and what is local. This provides difficulties for consumers to separate what they see on a documentary to what happens on farm. In the longer term, there has been a significant rise in the desire from consumers to see businesses tackle environmental topics, with the agricultural industry not alone in being urged to promote any environmental initiatives.

In recent years, concerns about the environment has led to a rise in meat-free products as the majority of consumers believe a vegan diet is more environmentally friendly. However, during lockdown, the number of households buying meat-free dropped by almost two percentage points – while the number of households buying red meat grew in comparison.

This is clearly welcome news for our livestock sectors, although experts warn that reductions may be temporary. In what is still a relatively small market, the meat-free sector is expected to grow in the longer term.

Looking ahead

We know that a lot of the shifts in buying behaviours are the result of the pandemic and while red meat had a reprieve from negative media coverage and enjoyed a year of strong growth, concerns around reputational issues have not disappeared and will rise back up consumer’s radar in the long term.

It is vital that industry addresses concerns around the environment, communicates the nutritional benefits of red meat as well as promoting the high welfare and quality of buying British. Simultaneously consumers will also be adjusting to 2021 in the backdrop of a hard economic reality that will start to influence behaviour changes in British homes. AHDB combine the evidence on consumer demand with how product supplies are changing to produce a forward picture to produce Agri-Market Outlooks. These can be found here https://ahdb.org.uk/agri-market-outlook

Behaviours characteristics to watch as economic ripple effect takes shape

- Consumers seeking value – Heavy price focus, strong value for money. Desire for households to make good use of leftovers/reduce waste.

- Scratch cooked, family meals – Increased likelihood of families building on this year’s experiences of cooking and eating together more frequently – which will also be more economical.

- Snacking/comfort through food – Taste, convenience and enjoyment are critical purchase drivers. Health considerations likely to rise on consumers agendas once uncertainty eases but communicating the nutritional benefits of eating red meat remain important.

To keep up-to-date with all the latest consumer retail trends, visit https://ahdb.org.uk/retail-and-consumer-insight